Popular Searches

Electric power is the "barometer" of national economic development, which can directly reflect the operation of the national economy. 2024 is a key year to achieve the goals and tasks of the "14th Five Year Plan" electric power planning, as well as a year of great development and breakthroughs in electric power. The overall balance of power supply and demand throughout the year is basically balanced, and the green and low-carbon transformation continues to advance. By the end of the year, the country's cumulative installed capacity of power generation had reached 3.35 billion kilowatts, an increase of nearly 15% year on year, reaching the "big pass" of 3 billion kilowatts installed capacity for the first time, achieving a historic leap, and the background of going green and becoming "new" has become increasingly strong. 2025 is the end year of the 14th Five Year Plan and the layout year of the 15th Five Year Plan. In the face of the increasingly complicated international situation, the increasingly arduous domestic reform and development tasks, and the increasing uncertainties and other challenges, China's power development is still full of expectations. New energy is still the "main force" of power development. The annual scale of new power generation is expected to be more than 400 million kilowatts, and China's power will usher in a greener, smarter and more sustainable future, In order to achieve the perfect "end" of the high-quality development of the "14th Five Year Plan" energy and power planning.

Overview of China's electric power development in 2024

In 2024, China's power development will generally show the characteristics of "fire", "water", "wind", "light", "nuclear", "production", "storage", and "hydrogen". In addition to the third largest nuclear power installation in operation in the world, China's installed capacity of fire, water, wind, light, production, and storage will all rank first in the world, making it the world's largest energy power country, It also provides a strong power guarantee for the national economic and social development and the people's good life.

"Fire" and "Water" increase simultaneously

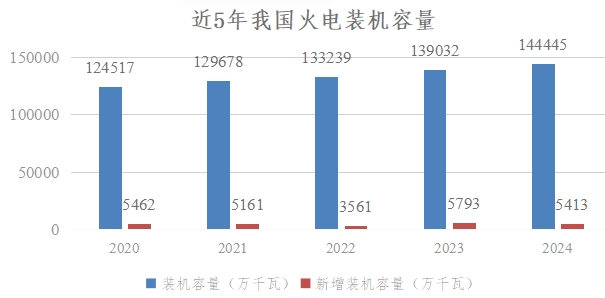

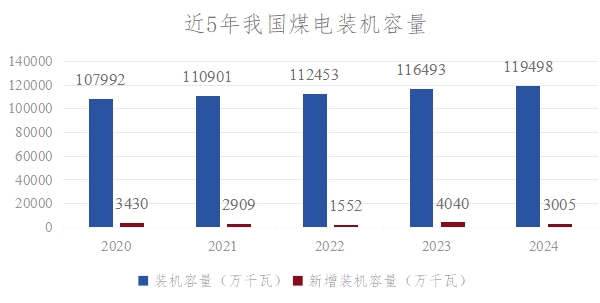

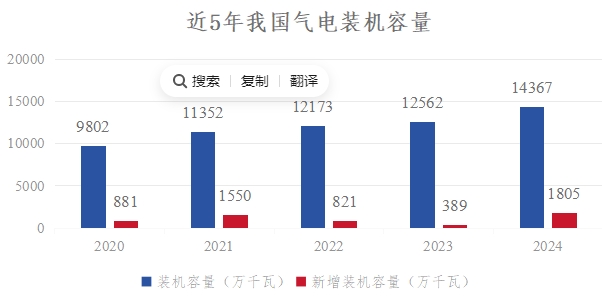

As a prominent representative of traditional energy power generation, thermal power (including coal power and gas power) and hydropower have achieved steady growth in 2024. By the end of the year, the installed capacity of thermal power had reached 1.444 billion kilowatts, accounting for 43.14% of the total installed power capacity in China, an increase of 3.8% over the new installed capacity of 54.13 million kilowatts in 2023, but the proportion of the installed capacity of thermal power in the total installed power capacity of the country decreased from 77.73% in 2007 to 44.14% in 2024, of which, the installed capacity of coal power was 1.195 billion kilowatts, an increase of 2.6% over the same period last year, It accounted for 35.7% of the total installed power generation capacity, a year-on-year decrease of 4.2 percentage points. The annual thermal power generation reached 6343.77 billion yuan, accounting for 67.36% of the total power generation (9418.06 billion kWh). It is the largest power source in China. On the whole, thermal power in China contributes nearly 70% of the power generation from less than half of the installed capacity. It can be seen that in the future and for a long time, thermal power, as the "key needle" of China's power supply, will play a key role of "ballast" in China's power and energy supply.

Thermal power generation:

Among them,Coal fired power generation:

Gas power generation:

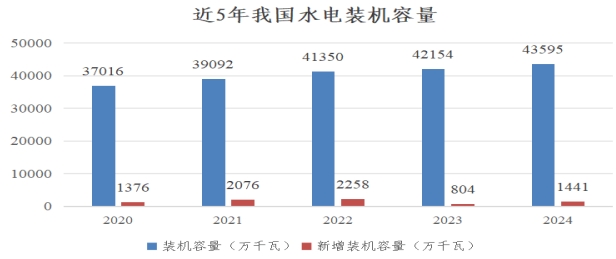

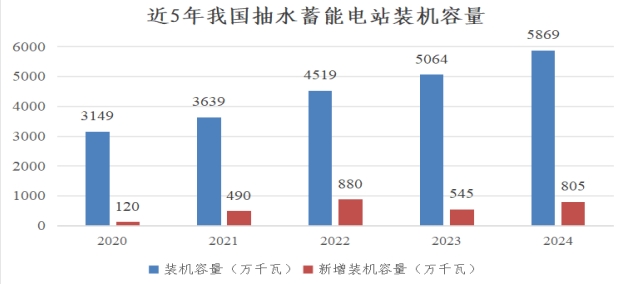

As the only renewable energy in conventional power, hydropower will show a steady growth trend in 2024, and maintain a leading position in the world. By the end of the year, the total installed capacity of hydropower in China had reached 436 million kilowatts, accounting for 13.02% of the total installed capacity of power in China, an increase of 3.2% compared with the new installed capacity of 13.78 million kilowatts in 2023, including 377 million kilowatts of conventional hydropower, an increase of 6.25 million kilowatts; The installed capacity of pumped storage is 58.69 million kilowatts, an increase of 7.53 million kilowatts year-on-year. The annual hydropower generation capacity was 1423.9 billion kWh, accounting for 13.53% of the total power generation, ranking second only to thermal power; The average annual utilization hours of hydropower above designated size are 3349 hours. Under the background of dual carbon goals and rapid development of new energy, hydropower, with its stable and clean characteristics, has become a reliable guarantee of clean energy supply in China.

Hydropower:

Among them,Pumped storage:

"Wind" and "Light" shine

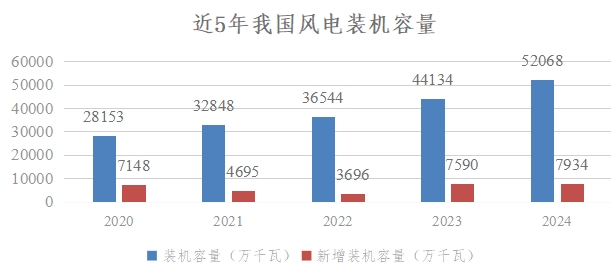

In 2024, wind power generation and photovoltaic power generation will be another big year. The cumulative new installed capacity of wind power generation throughout the year will reach 358 million kilowatts, accounting for 82.6% of the total new installed capacity of power generation throughout the year, which will exceed 293 million kilowatts in 2023. It is the first year in history that the new installed capacity will exceed 300 million kilowatts. The total installed capacity of Fengguang reached 1.41 billion kilowatts, historically exceeding that of coal power; The total amount of power generation totaled 1.83 trillion kilowatt hours, which was basically the same as the electricity consumption of the tertiary industry (1834.8 billion kilowatt hours) in the same period, and far exceeded the domestic electricity consumption of urban and rural residents (1494.2 billion kilowatt hours) in the same period, showing the strong vitality of wind power generation in China's energy substitution.

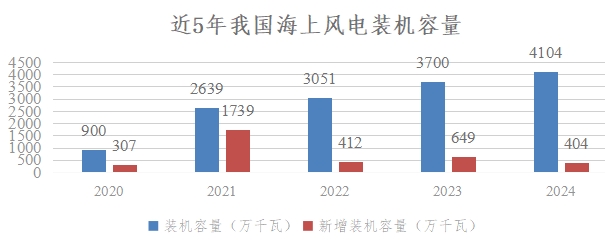

By the end of 2024, the cumulative grid connected capacity of wind power in China has reached 521 million kilowatts, an increase of 18% year on year, including 480 million kilowatts of onshore wind power and 41.27 million kilowatts of offshore wind power, ranking third in the installed capacity of power in China. The newly installed capacity throughout the year was 79.82 million kilowatts, up 6% year on year, including 75.79 million kilowatts of onshore wind power and 4.04 million kilowatts of offshore wind power. From the distribution of new installed capacity, the "three north" area accounts for 75% of the new installed capacity in China. In 2024, the national wind power generation capacity will be 991.6 billion kWh, with a year-on-year growth of 16%, ranking third only after thermal power and hydropower; The utilization hours of grid connected power generation throughout the year were 2127 hours, with an average utilization rate of 95.9%.

Wind power generation:

Among them,Offshore wind power:

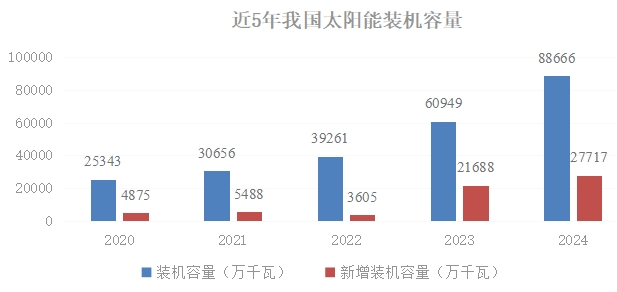

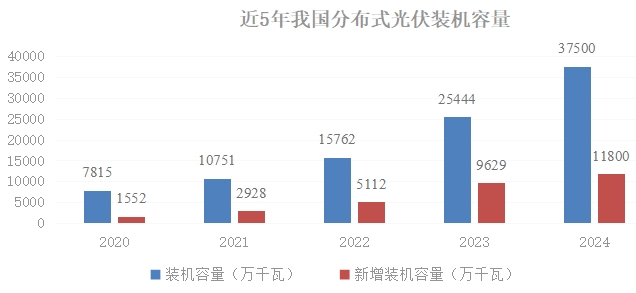

By the end of 2024, the installed capacity of photovoltaic power generation in China has reached 886 million kilowatts, a year-on-year increase of 45%, ranking second behind thermal power, including 511 million kilowatts of centralized photovoltaic power and 375 million kilowatts of distributed photovoltaic power. The new installed capacity of PV throughout the year was 278 million kilowatts, a year-on-year increase of 28%, including 159 million kilowatts of centralized PV and 118 million kilowatts of distributed PV. The annual photovoltaic power generation reached 834.1 billion kilowatt hours, up 44% year on year, but still lagging behind that of nuclear power, ranking fifth. The number of power generation utilization hours in the whole year was 1211 hours, and the utilization rate of power generation on grid was 96.8%, lower than that of the previous year.

Photovoltaic power generation:

Among them,Distributed PV:

Nuclear" and "Health" are mutually beneficial

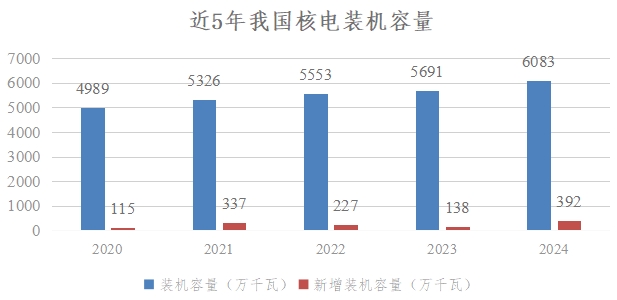

2024 is a milestone year for the development of nuclear power in China, with 11 new nuclear power units approved throughout the year, the highest number approved over the years, and more than 10 units approved for three consecutive years; Two sets of nuclear power generating units were put into operation, and the newly increased rated installed capacity was 2.4 million kilowatts; There are 102 nuclear power units in operation, under construction and approved to be built, with a total installed capacity of 113 million kilowatts, ranking first in the world for two consecutive years. By the end of the year, there were 57 nuclear power units in operation nationwide (excluding Taiwan), with a rated installed capacity of 59.4317 million kilowatts. The annual cumulative nuclear power generation capacity was 445.175 billion kilowatt hours, up 2.72% over the same period of the previous year, accounting for 4.73% of the national cumulative power generation, exceeding the solar power generation capacity and ranking fourth. It can be seen that the nuclear power installed capacity in China accounts for less than 2% of the total installed capacity in the country, but the electricity generated is close to 5% of the total power generation in the country. The annual equipment utilization hours are 7805.74 hours, and the average unit capacity factor is 90.26%.

Nuclear power:

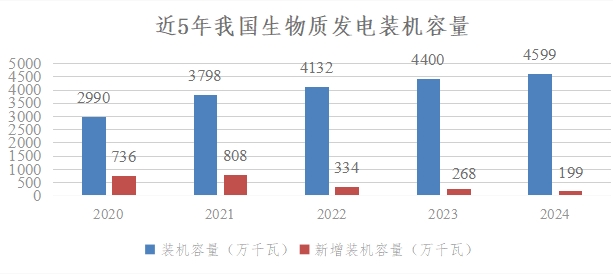

By the end of 2024, China's installed capacity of biomass power generation has reached 45.99 million kilowatts, of which 1.85 million kilowatts will be added in 2024, an increase of 4% year on year, ranking first in the world for six consecutive years. The cumulative power generation of biomass throughout the year was 208.3 billion kWh, up 5% year on year. Although biomass power generation in China is insignificant compared with other types of electricity, a new ecological energy system based on biomass is being built, which has initially formed a diversified development pattern with power generation as the main and non fuel energy such as bio natural gas and clean heating as the auxiliary. According to the research data of authoritative institutions, the development potential of biomass energy in China is about 460 million tons of standard coal. At present, the actual amount of coal converted into energy is less than 60 million tons of standard coal, which has great development potential.

Biomass power generation:

"Storage" and "Hydrogen" Progress Together

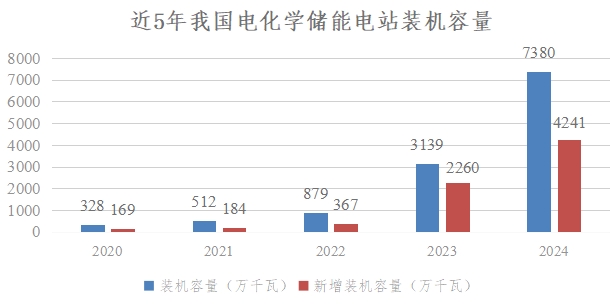

In 2024, China's new energy storage extended the strong development trend in 2023 and doubled again. By the end of the year, the cumulative installed capacity of new energy storage in China had reached 73.76 million kW/168 million kWh, an increase of more than 130% over the end of last year. The installed capacity of new energy storage put into operation in the whole year was 4370 kW/109.8 million kWh, up 103%/136% year on year. The cumulative installed capacity of new energy storage exceeded that of pumped storage for the first time, accounting for 57.6%; Among the new energy storage technologies, lithium-ion battery energy storage has become the energy storage technology with the highest market share, accounting for 55.2% of the total installed capacity of energy storage, followed by molten salt heat storage (0.8%), compressed air energy storage (0.6%), and liquid flow battery (0.4%). In particular, 2024 will be a year when China's new energy storage will make a breakthrough. The world's first 300MW compressed air energy storage demonstration project, "Energy Storage No.1", will be connected to the grid in full capacity, the first 100 megawatt full vanadium liquid flow battery shared energy storage power station in severe cold regions will be officially put into operation, and the first independent flywheel energy storage power station will be successfully connected to the grid, from "one flower stands out" to "many flowers bloom".

Electrochemical energy storage:

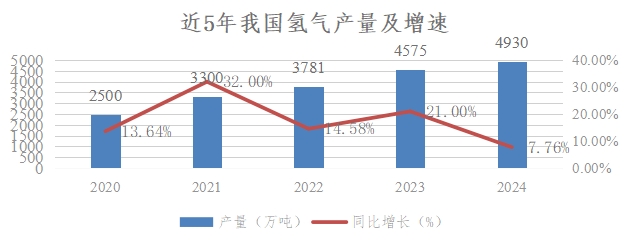

In 2024, the scale of China's hydrogen energy industry will continue to expand. By the end of the year, more than 100 green hydrogen projects had been completed in China, and the renewable energy hydrogen production capacity had exceeded 120000 tons/year, doubling from the end of 2023; 540 hydrogenation stations have been built, ranking first in the world; The megawatt proton exchange membrane hydrogen electricity integration station, electricity hydrogen coupled DC microgrid, island hydrogen utilization and other demonstration projects have been completed successively, and the core hydrogen storage equipment is entering the substantive application stage; The scale of public bidding for electrolytic water hydrogen production equipment in the whole year exceeded 2.2GW, with a year-on-year growth of about 30%; Anhui Lu'an Hydrogen Storage Power Station of the State Grid achieved 4-hour peak shaving response, and the cost per kilowatt hour dropped to 0.42 yuan, 18% lower than the lithium battery; More than 400 green hydrogen projects are planned to be built accumulatively, the demand for electrolytic cells reaches 72 GW, and the planned green hydrogen capacity exceeds 8 million tons/year.

Hydrogen production:

Prospects for China's electric power development in 2025

2025 is the tenth year of the new round of power system reform and the beginning year of the comprehensive marketization of new energy. According to the Guiding Opinions on Energy Work in 2025 recently issued, the total installed capacity of power generation across the country will reach more than 3.6 billion kilowatts, the newly added installed capacity of new energy power generation will reach more than 200 million kilowatts, the generating capacity will reach about 10.6 trillion kilowatt hours, the installed proportion of non fossil energy power generation will increase to about 60%, and the proportion of non fossil energy in total energy consumption will increase to about 20%, And a national unified power market has been initially established. It can be seen that China's power development is accelerating the transformation from "scale expansion" to "quality and efficiency leap", showing the characteristics of "coal", "gas", "water", "calm waves," wind "," rain "," light "," shadow "," nuclear "," new "," life "," storage ", and" hydrogen ". The" inflection point "of power transformation is coming.

"Coal" and "Gas" Show:On the one hand, the development space of thermal power in China is squeezed due to the aggressive impact of new energy. However, with the help of the "three 80 million" policy of coal power, the installed capacity of thermal power is expected to rise slowly in the future, but the growth rate of gas power is higher than that of coal power; On the other hand, although the role of thermal power as "ballast" will not change in the short term, it will gradually shift from "base load power supply" to "regulating power supply", and support the consumption of renewable energy through flexibility and clean transformation (such as improving peak shaving capacity), and the utilization hours of power generation will be reduced year by year. In 2025, the installed capacity of thermal power in China is expected to be about 1.5 billion kilowatts, of which the installed capacity of coal power is expected to be about 126000 kilowatts, falling to about 1/3 of China's total installed capacity for the first time. In addition, in the future, the focus of China's thermal power investment will be to promote projects under construction and nuclear projects to be put into production quickly, and to strengthen flexibility, energy conservation and clean carbon reduction transformation will become an important area of thermal power investment. The "ceiling" of coal power development is approaching.

"Water" is flat and the waves are still: Since most of the hydropower stations with development conditions in China have been completed, the remaining hydropower stations that have not been developed are mainly located in Tibet, Yunnan, Guizhou, Sichuan and other southwest regions, facing the natural conditions of high slopes, high elevations, large temperature differences and other complex areas of high mountains and deep valleys, as well as higher technical requirements and stricter environmental protection standards, the difficulty of development has increased significantly, It limits the growth rate of new installed capacity. However, with the launch of hydropower development in Yaxia Basin and the rise of pumped storage power stations, China's hydropower development will continue to advance in an orderly manner in 2025, in which the installed capacity of pumped storage will grow faster than that of conventional hydropower. The installed capacity of hydropower is expected to be around 450 million kilowatts, and the new installed capacity of hydropower will be basically the same as that of 2024. Driven by pumped storage, The annual investment scale of China's hydropower industry is expected to remain above 100 billion yuan.

"Wind" regulating rain order: Stimulated by Document No. 136, China's wind power will usher in a new wave of "rush to install" before May 31 this year. Based on the new energy indicators generated underground in 2024, 2025 is very likely to become the "big year" of China's wind power development, ushering in an intensive period of completion and online access. It is estimated that the annual new wind power installed capacity will exceed 100 million kilowatts for the first time, At the end of the year, the total installed capacity of grid connected wind power was about 650 million kilowatts, accounting for about 17% of China's total installed capacity. In particular, with the introduction of the "single 30" standard for sea wind on December 23, 2024, it is expected to truly solve the problem that has long plagued the development and use of sea power for far-reaching sea wind energy resources, fundamentally change the depressed construction status of offshore wind power for three consecutive years since the rush to install in 2021, and become the focus of future new energy development in China's coastal areas. The new installed capacity of offshore wind power in 2025 is expected to be about 15 million kilowatts, which is expected to reach another "high point" of the new installed capacity of offshore wind power in 2021.

"Light" and shadow interlace:The year 2024 can be described as "five flavors mixed" for China's photovoltaic power generation: on the one hand, the installed scale of photovoltaic power generation has reached a new historical high; on the other hand, overcapacity and vicious competition at low prices have seriously led to huge losses in the entire industry chain. In 2025, under the influence of No. 136 document, China's photovoltaic power generation will usher in a wave of "rush to install" in the first half of the year like wind power, but the newly added photovoltaic power generation capacity may not be as large as that of last year. By the end of 2025, it is estimated that the grid connected solar power generation capacity will be around 1.1 billion kilowatts, accounting for 29% of China's total installed power capacity. In particular, with the industrial and commercial industry canceling full access to the Internet and the project above 6MW can only be used by itself and other policy changes, distributed photovoltaic has brought uncertainty. It is expected that 2025 will not be as "hot" as 2024, and the installed capacity will face a slowdown trend. However, the development prospect of offshore photovoltaic is very broad, and it is likely to usher in the "first year" of the outbreak.

"Nuclear" is new:Since the restart of nuclear power in 2019, the pace of nuclear power development in China has significantly accelerated, and the scale of units in operation and under construction has jumped to the top in the world. The "Hualong No.1" demonstration project has been fully completed and put into operation, and the "Guohe No.1" demonstration project unit 1 has been grid connected for power generation. The world's first fourth generation nuclear power plant, a high-temperature gas cooled reactor nuclear power plant, has been put into commercial operation, The installation work of the onshore commercial modular small nuclear reactor "Linglong No.1" has entered a peak period, marking that China's nuclear power technology has entered the world's leading level and contributed Chinese wisdom and Chinese solutions to the global nuclear power development. It is estimated that by the end of 2025, China's rated nuclear power installed capacity will reach about 65 million kilowatts. From 2022 to 2024, China's annual investment in nuclear power will increase by more than 50% on average. According to this growth rate, it is estimated that China's annual investment in nuclear power will reach about 200 billion yuan in 2025, almost twice the size of hydropower investment.

The other side of "Health":Although biomass energy is a "niche" energy variety in China, its green value has attracted much attention. Last October, the National Development and Reform Commission (NDRC) issued a civilized requirement that "biomass power generation should be developed steadily, and green fuels such as bio natural gas, bio diesel and bio aviation coal should be developed according to local conditions", and also explicitly proposed that coal power units should have the ability to blend more than 10% of biomass fuel. In addition to straw, garbage and biogas power generation, green methanol and sustainable aviation fuel (SAF) will become new ways of biomass energy application. In addition, small biomass cogeneration projects and the construction of "zero carbon parks" will blossom in many places to meet the demand of residents and parks for electricity and heating. By the end of 2025, it is expected that the installed capacity of electric materials in China will be about 48 million kilowatts, an increase of 2 million kilowatts over the previous year.

"Storage":As a necessary link to build a new power system, the new energy storage has expanded rapidly since the explosive growth in 2022, and achieved "triple jump" in three years. In 2024, it will surpass the traditional pumped storage for the first time and become the largest installed capacity of energy storage. In 2025, China's new energy storage will continue the previous high growth trend, and new application scenarios such as optical storage and charging integration will continue to expand. In the context of a significant increase in the installed capacity and power of renewable energy, networking technology will become an important development direction of the industry. By the end of 2025, the total installed capacity of China's new energy storage is expected to exceed 100 million kilowatts, and long-term energy storage technologies (such as liquid flow batteries, compressed air), hydrogen energy storage, etc. will receive more and more attention; Networked energy storage is accelerating towards industrial landing, and the annual shipment is expected to reach 7GW; solid state batteries, nano ion batteries, high-temperature cells, etc. are expected to usher in new breakthroughs.

"Hydrogen" song and slow dance:The Energy Law has included hydrogen energy in the list of energy, which has removed legal obstacles to the development of hydrogen energy. After years of technology accumulation, precipitation and commercial demonstration exploration, China's hydrogen energy, especially green hydrogen, demand market is becoming larger and larger, and hydrogen energy applications are becoming more and more scene oriented. Some highly mature integrated projects such as hydrogen ammonia alcohol may become anchors for industrial transformation. In 2025, China's hydrogen energy industry will usher in a rush period of large-scale production. By the end of the year, it is expected that the capacity of electrolytic water hydrogen production will reach about 300000 tons/year, and the installed capacity of hydrogen energy storage is expected to exceed 2GW. At the same time, the application of hydrogen energy in industries, distributed power generation, energy storage and other fields has continued to expand, and the application scenarios of hydrogen blending from coal, hydrogen production from sea breeze, liquid hydrogen production, filling and hydrogen fuel vehicles have become more abundant, jointly promoting the scale of the hydrogen energy industry to the trillion yuan mark, and becoming a new engine for green growth of the national economy.

010-67184197、13311211762

dtly@datonglongyuan.com

Room E1-301, Oriental Plaza, No.1 East Chang' an Avenue, Dongcheng District, Beijing, China

Follow The Official WeChat Account