Popular Searches

The weekly report of CECI Index Analysis (the 8th issue in 2025) released by the preparation office of China Electricity Coal Purchase Price Index (CECI) shows that the spot transaction price of high calorific value coal in the CECI Coastal Index continues to decline significantly. The Caofeidian index continued to accelerate downward. The spot transaction price of import index high calorific value specification coal increased. The CECI purchasing managers' index has been in the contraction range for eight consecutive periods. In sub indexes, all sub indexes continue to be in the contraction range. The supply, demand and shipping sub indexes have increased month on month, while the inventory and price sub indexes have decreased month on month.

Market overview

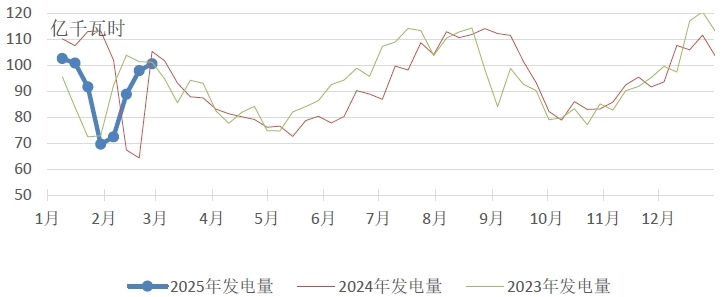

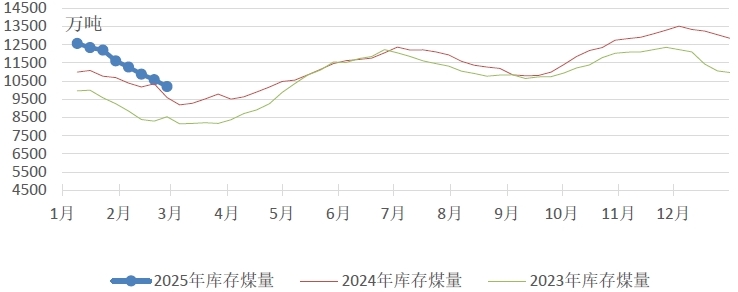

In terms of production of coal-fired power plants, downstream enterprises have resumed work in succession, and the power generation and coal consumption have increased month on month. Recently, the temperature in most regions has continued to warm up, and the heat supply is basically flat month on month. Most coal power enterprises focus on just in need procurement and de stocking. The coal inflow is basically flat month on month, and the inventory continues to decline month on month, but the inventory and available days are still higher than the level of the same period last year. According to the fuel statistics of China Power Union, the average daily power generation of coal-fired power plants of power generation groups included in the fuel statistics of the power industry in the current period increased by 2.7% month on month and decreased by 4.5% year on year. The average daily heat supply decreased by 0.5% month on month and increased by 20.0% year on year. Average daily coal consumption for power generation increased by 1.7%, with a year-on-year decrease of 5.8%. Among them, the average daily coal consumption of sea transportation power plants increased by 4.1% month on month and 4.0% year on year; The average daily coal inflow increased by 13.7% month on month and 26.2% year on year. Coal storage of coal-fired power plants was 101.94 million tons, up 6.05 million tons year on year.

Figure 1 Trend of weekly average power generation of coal fired power plants

Figure 2 Trend of Coal Inventory in Coal fired Power Plants

In terms of the main coal producing areas in China, most of the coal mines maintain normal production. The state-owned coal mines are still mainly responsible for ensuring the long-term cooperative shipment and internal supply. Some coal mines temporarily shut down due to safety inspection, but the overall coal supply is basically stable. Affected by the continuous decline in port prices, the surrounding coal plants and traders were relatively cautious in purchasing, and the actual market transactions were few. Except for the small increase in the sales price of lump coal in some regions, the spot price of the pithead market was weak and stable.

In terms of port market, the overall procurement demand of downstream enterprises is weak, the speed of port destocking is slow, and the pressure of port dredging continues to exist. Most market participants believe that the coal price has not yet bottomed out, and the bearish sentiment continues to spread. The market operation is more cautious and wait-and-see. The market inquires about goods and prices less. The purchase is dominated by low prices. The spot transaction price continues to decline, and the decline is further expanded.

To sum up, some coal mines have reduced production or reduced prices to digest high inventory, and the supply of coal from main coal producing areas is relatively stable. Downstream construction resumed in succession, power generation and coal consumption continued to rise, power plant inventory was still at a high level, and there was no significant increase in market demand for coal procurement at this stage. Market prices continue to bear pressure, and spot transaction prices at pitheads and ports continue to operate in a weak position.

CECI index analysis

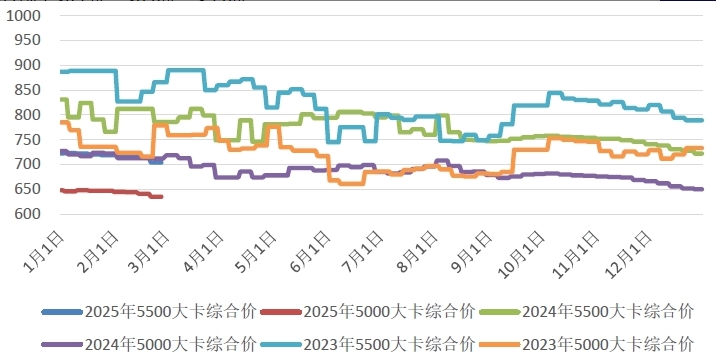

The spot transaction prices of the CECI Coastal Index 5500 kcal/kg and 5000 kcal/kg decreased by 33 yuan/ton and 20 yuan/ton respectively compared with the previous period, and the decline range increased by 20 yuan/ton and 5 yuan/ton respectively compared with the previous period. From the sample situation, the sample price ranges of spot transaction prices of 5500 kcal/kg and 5000 kcal/kg specifications are 708-713 yuan/ton and 621-646 yuan/ton respectively. From the distribution of sample calorific value, 4500 kcal/kg, 5000 kcal/kg and 5500 kcal/kg samples accounted for 40.5%, 42.3% and 17.2% of the total respectively.

Figure 3 CECI Coastal Index Composite Price Trend Chart

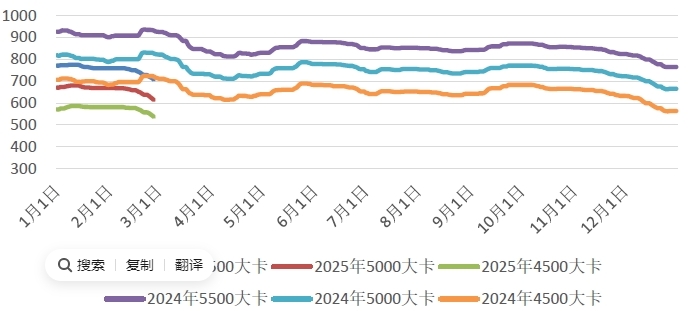

The average prices of the CECI Caofeidian Index 5500 kcal/kg, 5000 kcal/kg and 4500 kcal/kg were 717.8 yuan/ton, 626.4 yuan/ton and 548.2 yuan/ton, respectively. The spot price of power coal continued to accelerate downward, and the average prices of various specifications this week were 24.4 yuan/ton, 25.4 yuan/ton and 22.6 yuan/ton lower than last week. The average number of spot transactions increased slightly, including 5000 kcal/kg, 5500 kcal/kg and 4500 kcal/kg samples.

Figure 4 Trends of CECI Caofeidian Index

The unit price of landed standard coal in the CECI import index was 854 yuan/ton, up 4 yuan/ton from the previous period and 0.5% month on month. Among spot prices, except for Guangzhou Port (Panama type) with a stable price of 3800 kcal/kg, the spot price of imported coal with calorific value of various specifications rose and fell differently, including Taicang Port (Handy type) with a price drop of 49 yuan/ton month on month, and Guangzhou Port (Panama type) with a price drop of 32 yuan/ton month on month. Influenced by factors such as rainfall in Indonesia and the coming Ramadan, foreign mines are still willing to support the price of low calorie coal. Some domestic coastal power plants continue to release long-term procurement demand. In addition, the price of international ocean freight continues to rise, the pressure on import traders to purchase remains, and the focus of low calorie coal bidding price moves upward. As the decline of coal price in the domestic market has expanded, combined with the continuous weakness of domestic demand for high calorie coal, the sales pressure has led to the continuous reduction of the overall quotation range of Russian coal, Australian coal and other mines for high calorie coal, and the decline of coal price has expanded.

Table 1 CECI Import Index

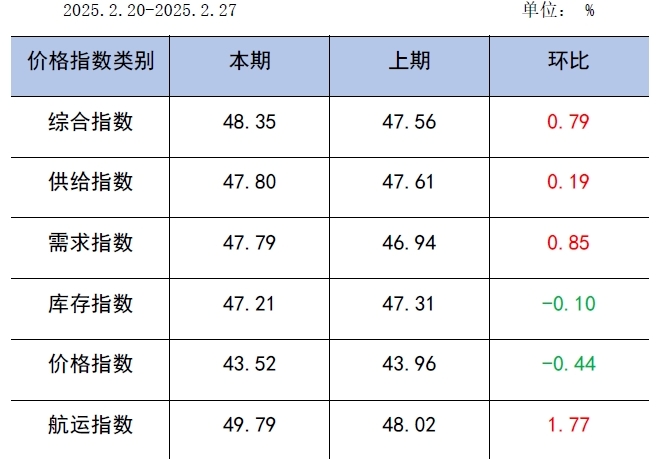

The CECI purchasing managers' index was in a contraction range for eight consecutive periods. Among them, the supply sub index has been in the contraction range for 8 consecutive periods, indicating that the supply of power coal continues to decline, and the decline has narrowed. The demand sub index has been in the contraction range for eight consecutive periods, indicating that the demand for thermal coal continues to decline and the decline has narrowed. The sub index of inventory has been in the contraction range for 8 consecutive periods, indicating that the inventory of thermal coal continues to decline and the decline has expanded. The price sub index has been in the contraction range for six consecutive periods, indicating that the price of thermal coal continues to decline and the decline has expanded. The shipping sub index has been in the contraction range for 12 consecutive periods, indicating that the price of thermal coal shipping continues to decline, and the decline has narrowed.

Table 2 CECI Purchasing Manager Index

Relevant information and suggestions

According to the monitoring and summary data of the Leading Group Office of the State Council for Logistics, from February 17 to February 23, the national freight logistics operated in an orderly manner, including 76 million tons of goods transported by national railways, an increase of 1.7% month on month; There were 48.55 million trucks on expressways nationwide, up 17.47% month on month.

According to the power industry fuel statistics of China Power Union, as of February 27, the cumulative power generation of coal-fired power plants included in the statistics increased by 7.8% year on year in this month and decreased by 7.4% year on year in this year. The coal consumption of coal-fired power plants increased by 5.9% year-on-year in this month and decreased by 6.0% year-on-year in this year. The coal inventory of coal-fired power plants was 6.05 million tons higher than that of the same period last year, and the number of days available for inventory was 1 day higher than that of the same period last year.

Recently, most domestic industrial fields have resumed production in an all-round way, the operating rate of enterprises has continued to increase, the daily consumption of coastal power plants has continued to increase, and the inventory of power plants has remained depleted. On the one hand, although the port has taken measures to promote de stocking, the inventory of northern ports is still high except Huanghua Port. With the heating season in the north coming to an end in March, downward pressure on coal prices still exists in the traditional slack season, and the market trading atmosphere remains cold. On the other hand, after the conclusion of the national major conference, the macroeconomic environment is expected to gradually improve, the process of infrastructure and chemical industry resumption will be accelerated, and the demand for coal in the non power industry is expected to gradually increase, or drive the continued de stocking of port stocks. At the same time, the measures taken by some power generation enterprises to suspend the purchase of imported coal may promote the acceleration of the process of removing domestic trade coal from storage and push the price of steam coal market to bottom. Based on comprehensive judgment, the short-term steam coal market will remain weak. According to the forecast of the meteorological department, affected by the cold wave, there will be a wide range of rain, snow and strong wind cooling weather in the central and eastern regions from March 1. It is suggested that first, power enterprises should do a good job in ensuring the supply of energy and electricity during the National "Two Sessions"; Second, pay attention to the implementation of the Indonesian government's policy of requiring HBA price index for global trade pricing and its impact on China's coal imports, and study and adopt countermeasures.

010-67184197、13311211762

dtly@datonglongyuan.com

Room E1-301, Oriental Plaza, No.1 East Chang' an Avenue, Dongcheng District, Beijing, China

Follow The Official WeChat Account